PREC Accounting in Ontario: A Complete Guide for Real Estate Agents

How Ontario realtors use a PREC to tax commissions at 11.2% instead of up to 53.53%: who qualifies under TRESA, salary vs dividends, HST and bookkeeping changes, running costs, and when incorporating is not worth it.

A Personal Real Estate Corporation (PREC) lets an Ontario real estate agent run commission income through a corporation that pays 11.2% combined tax on its first $500,000 of active business income as of July 1, 2026, instead of personal rates that climb to 53.53%. Any salesperson or broker registered with RECO has been allowed to set one up since October 1, 2020, under the Trust in Real Estate Services Act (TRESA). The catch: a PREC defers tax rather than eliminating it, so it only pays off when you consistently earn more than you spend.

Who can set up a PREC in Ontario?

Every RECO-registered salesperson and broker qualifies. The structure is governed by Ontario Regulation 536/20 under TRESA, and the conditions are strict but simple:

- The corporation is incorporated under the Ontario Business Corporations Act.

- You, the registrant, are the sole controlling shareholder and own all of the equity (voting) shares.

- You are the sole director and the sole officer.

- You and your family members, meaning your spouse, children and parents, may hold non-equity (non-voting) shares directly; a trust may hold them only on behalf of your minor children.

- The PREC cannot trade in real estate itself. Its only permitted activity on the brokerage side is supplying your services to your brokerage, and neither you nor the PREC may advertise that the corporation trades in real estate.

- Your commissions must flow from the brokerage to the PREC. You cannot receive trading remuneration from anyone other than your PREC or your brokerage.

The PREC itself does not register with RECO. You do, however, have to give RECO the corporation's legal name and address for service before it receives its first dollar of commission, and sign the required agreement between you, the PREC and your brokerage.

How much tax does a PREC actually defer?

This is the whole reason PRECs exist. A Canadian-controlled private corporation pays the combined federal and Ontario small business rate on its first $500,000 of active business income. Ontario cut its portion from 3.2% to 2.2% effective July 1, 2026, so the combined rate dropped from 12.2% to 11.2% (prorated for corporate year-ends that straddle that date). The federal small business rate stays at 9%, per the CRA's corporation tax rate tables. Income above $500,000 is taxed at the combined general rate of 26.5%.

Compare the marginal rates, meaning the tax on the next dollar earned, under 2026 Ontario rules:

| Where the next dollar is taxed | 2026 marginal rate | Tax per $100,000 at that rate |

|---|---|---|

| PREC, small business rate (from July 1, 2026) | 11.2% | $11,200 |

| PREC, income above $500,000 | 26.5% | $26,500 |

| Personally, in the $150,000 to $181,440 bracket | 44.97% | $44,970 |

| Personally, in the top bracket (over $258,482) | 53.53% | $53,530 |

The per-$100,000 figures illustrate each rate; personal income that spans more than one bracket pays a blended amount. For an agent already past the top bracket, every $100,000 left inside the PREC keeps roughly $42,300 more working capital than earning the same amount personally. Retain $250,000 in a strong year and the corporation pays about $28,000 of tax where you would have paid about $133,800 personally. That difference can sit in investments, pay down the corporation's expenses or smooth out a slow market.

Be clear about what this is: a deferral. When you eventually pull retained earnings out as dividends, personal tax applies at that point, and Canada's integration rules are designed so the combined corporate-plus-personal bill lands within about a point of what salary would have cost. The real wins come from timing, such as paying yourself in retirement or in low-income years at far lower brackets, and from investing pre-tax dollars in the meantime.

Should you pay yourself salary or dividends from a PREC?

When salary makes sense

Salary is deductible to the PREC and creates RRSP room: 18% of earned income, up to the $33,810 dollar limit for 2026, which takes roughly $188,000 of prior-year salary to max out. It also builds CPP entitlement. The cost is payroll administration plus both halves of CPP, about $9,300 combined at 2026 maximums ($4,230.45 each on earnings to $74,600, plus $416 each in CPP2 contributions on earnings to $85,000).

When dividends make sense

Dividends from a PREC are non-eligible dividends. At the 2026 top bracket they cost 47.74% personally, but at moderate incomes they are cheaper than at the top: at around $120,000 of total income, the 2026 marginal rate on non-eligible dividends is about 36% (36.10%), and it falls to roughly 25% (25.16%) once taxable income is below about $112,000. There is no CPP to pay and no payroll remittances to run, but you build no RRSP room and no CPP pension. Note that Ontario is cutting its non-eligible dividend tax credit from 2.9863% to 1.9863% on January 1, 2027, which nudges dividend costs up slightly to match the lower corporate rate.

What most agents actually do

A common structure is a salary large enough to generate RRSP room and CPP, topped up with dividends as cash needs arise. The right mix depends on your age, spending, mortgage plans and pension goals. Our comparison of dividends versus regular income in Canada walks through the trade-offs in more detail.

What changes for bookkeeping and HST when you incorporate?

A PREC is a new legal person, and the CRA treats it that way from day one:

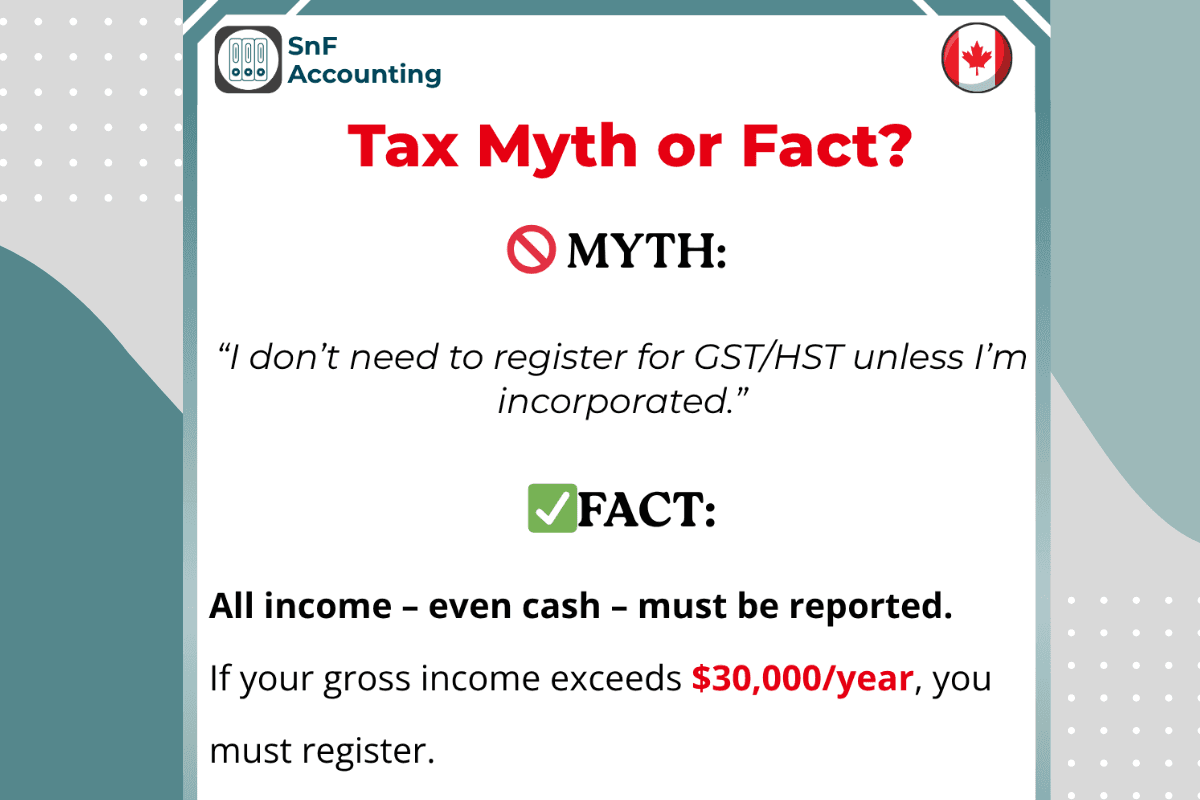

- New GST/HST number. Your personal registration does not transfer. The small supplier threshold is $30,000 of taxable supplies in a single calendar quarter or over four consecutive quarters, and you must register within 29 days of crossing it. Most agents pass $30,000 almost immediately, so register the PREC before the first commission lands. Commissions in Ontario carry 13% HST, and we cover the mechanics in our guide to HST on real estate commissions in Ontario.

- Separate books and bank account. The PREC needs its own account, and every expense should run through it. Mixing personal and corporate spending is the fastest way to lose deductions in an audit.

- A T2 corporate return. It is due six months after your corporate year-end, but tax owing is due three months after year-end for a CCPC claiming the small business deduction. You can pick a non-calendar year-end.

- Payroll and slips. Paying yourself salary means a payroll account, monthly source deductions and a T4 by the last day of February. Dividends require a T5.

What does it cost to run a PREC?

Budget $1,500 to $3,000 to incorporate with a lawyer who gets the share classes right, since a PREC with the wrong structure is offside the regulation. Ongoing, a traditional firm typically charges $3,000 to $5,000 per year for corporate bookkeeping, the T2, HST filings and payroll. SNF Accounting handles all of that for real estate agents and PRECs on fixed pricing from $199 per month, so the carrying cost is known before you incorporate.

When is a PREC not worth it?

- You spend what you earn. If every commission dollar goes to living costs, nothing stays in the corporation at 11.2%, and you have added cost and paperwork for no deferral.

- Net commissions are modest. Below roughly $150,000 of net commission income, the amounts most agents can realistically retain rarely justify the setup and annual costs. Run the numbers rather than assuming.

- You are about to qualify for a mortgage. Lenders assess your personal income. Money parked in a PREC can shrink what you qualify to borrow.

- Large investment balances inside the corporation. Passive investment income above $50,000 grinds the $500,000 small business limit by $5 for every $1 over, and the limit disappears entirely at $150,000 of passive income.

Frequently Asked Questions

Can my spouse or children own shares in my PREC?

Yes, but only non-equity, non-voting shares. Ontario Regulation 536/20 restricts these to your spouse, children and parents holding directly (or a trust holding solely for your minor children). Do not assume this means easy income splitting: the federal tax on split income (TOSI) rules generally tax dividends paid to family members at the top marginal rate unless a narrow exception applies, and most realtor households do not meet one. Get advice before paying a family member a dividend.

Does my PREC need its own HST number?

Yes. The PREC is a separate legal entity, so your existing personal GST/HST registration does not carry over. Because real estate commissions are taxable supplies and almost every full-time agent exceeds the $30,000 small supplier threshold, the PREC should be registered before it receives its first commission. The brokerage then pays commissions plus 13% HST to the corporation, and the PREC claims input tax credits on its business expenses and remits the difference.

Do I need RECO's approval to set up a PREC?

No approval or PREC registration is required. The corporation is exempt from registration as long as it meets the conditions in the regulation, including the sole controlling shareholder rules and the ban on the PREC trading in real estate. You must notify RECO of the PREC's legal name and address for service before it receives any remuneration, and you, your PREC and your brokerage must sign a written agreement covering how commissions are paid.

Can my PREC hold rental properties or investments?

A PREC can invest its retained earnings in stocks, funds or real estate held for investment, because the restriction is on trading in real estate as a service for others, not on owning assets. Two cautions apply. Passive income above $50,000 per year starts eroding access to the 11.2% small business rate, and holding appreciating property inside a corporation can create worse tax outcomes on sale than personal ownership. Model it first.

Is a PREC worth it if I earn under $150,000?

Usually the case is weak, but it depends on retention, not revenue. An agent netting $140,000 who lives on $80,000 can retain meaningful money at 11.2% and may benefit. An agent netting $200,000 who spends $200,000 gains nothing. As a rough test, if you can leave at least $30,000 to $40,000 in the corporation each year, the deferral typically outruns the roughly $2,400 to $5,000 of annual carrying costs.

Thinking about incorporating, or already running a PREC that feels more expensive than it should be? Book a free 30-minute consultation with SNF Accounting. We are a CPA-led firm serving realtors across Ontario and the rest of Canada with fixed pricing from $199 per month, and we will tell you plainly whether a PREC makes sense at your numbers.